Simplified Guide for SECP Annual Filing in 2025

The next crucial step after registering a company. Companies must fulfil certain legal requirements to maintain their “active” status with the Securities and Exchange Commission of Pakistan (SECP).

Annual filing with SECP is as mandatory requirement for registration with several departments, for example registration with provisional Revenue Authority PRA, KPRA. Without it, registration with any department is not possible.Moreover, the State Bank of Pakistan (SBP) has also made it mandatory for companies to submit their annual returns or forms, and in case of non-compliance, it is not possible to open a new bank account in the name of the company.

Appointment of First Auditor

All companies with paid up capital exceeding PKR 1,000,000 are required to appoint their first auditor within 90 days of registration. A letter of consent is required from the auditor before Appointment. Here is the sample consent letter for the guideless purposes only.

Appointment of Legal Adviser:

Appointment of Legal Adviser:

Appointment of Legal Adviser:

Appointment of Legal Adviser:All Companies having paid up capital of more than Rs 7.5 million, limited by guarantee and all Associations registered under section 42 of the Act are required to immediately Appoint a legal advisor.

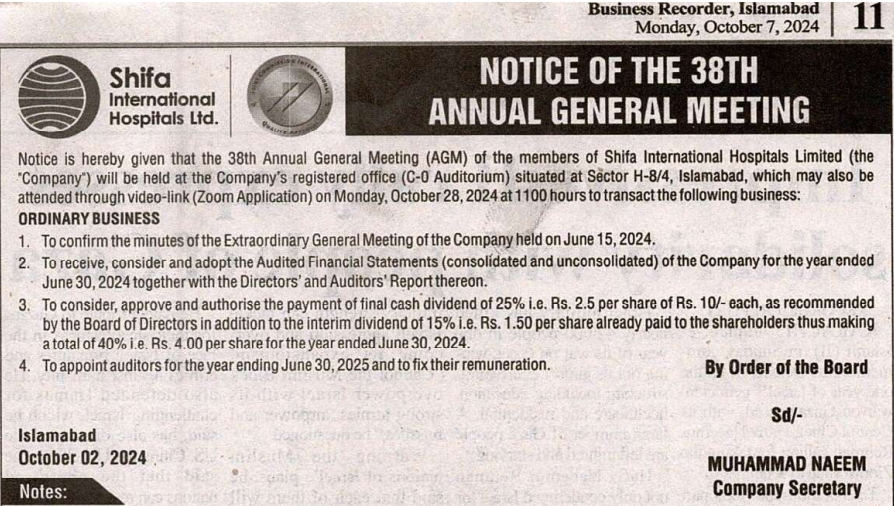

Annual General Meeting (AGM)

Annual General Meeting (AGM)

Annual General Meeting (AGM)

Annual General Meeting (AGM)Every private company is required to hold its first AGM within 16 months of incorporation and the next will have to be hold within 120 days after the end of financial year.

For example, if a Private Ltd. company is registered on 15 August 2022:

The 16 months period is completed on 13 December 2023 first AGM must be held before 13 December 2023

The second AGM must be held before 28 October 2024, if the financial year ends on 30 June

The financial year for most companies starts from 1 July and ends on 30 June. However, banks and financial institutions generally have the calendar year (1 January to 31 December).

Why holding of Annual General Meeting (AGM) is important?

Another question that often arises in the minds of people is why it is necessary for a company to hold a general meeting and for what purpose is it done? Especially in Pakistan, most companies are formed by family businesses or partnerships of a few friends

Most people think that since it is the family’s own company, what kind of meeting and what agenda is there in it? It is just paperwork, Form A and Form 9 are filed, consultation is done at home. Then what is the need for this formality?

Importance of AGM in large and Section 42 Companies

In large companies, there is a regular AGM, in which investors are involved, the future strategy, projects and performance of the company are discussed. Similarly, in non-profit organizations registered under Section 42, more transparency is necessary because they are run by donor money. In them, the directors are independent, and the financial and administrative affairs of the organization are fully examined in the meeting.

The general meeting is not just a formality.

Therefore, the holding of general meeting is not just a legal formality but important for the transparency, accountability and decision making of the company.

What matters are discuss Annual General Meeting (AGM)?

Whenever any important decision has to be taken in a company, it is necessary to hold a meeting of the Board of Directors. In this meeting, all the matters are discussed in detail. Some decisions are taken in the Annual General Meeting (AGM), while some emergency decisions are taken in the Extraordinary General Meeting (EOGM).

Generally, the following matters are included in the AGM:

- Appointment of auditor

- Amendment of the Memorandum or Articles of Association

- Approval of audited accounts

- Change of address or name of the company

- And other legal and administrative decisions

Need for Board Meetings for Important Decisions

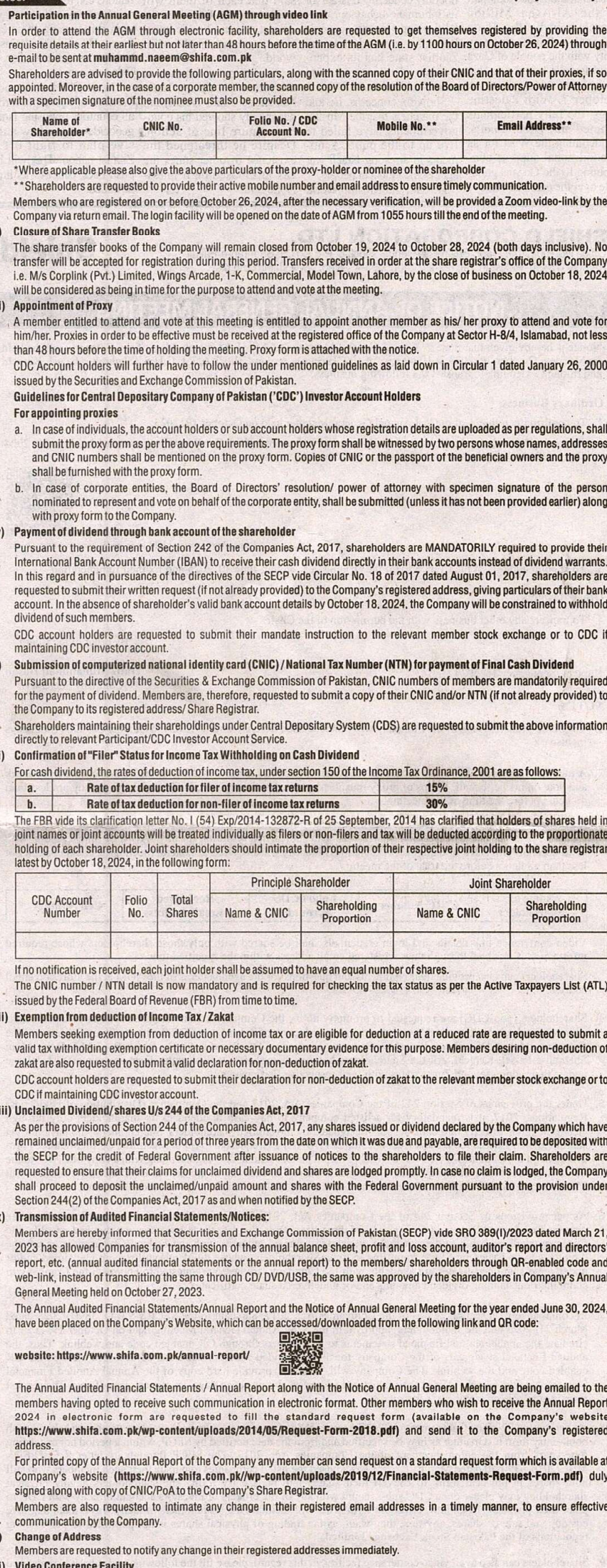

In addition, if the company has to change its bank account, change the Authorized Signatory, or submit any form to the SECP, then an approved resolution of the Board meeting is also required. No form will be acceptable without the approval of the Board. The form filed with the SECP must be accompanied by a resolution passed by the board, signed by all the directors.

Publication of Meeting Notices and Decisions

In the large or public interest companies must publish their meetings and decisions in newspapers to maintain transparency. A notice is issued before the meeting, stating the agenda, and after the decisions are made, they are published in regular newspapers.

Elections

Every company is required to hold its first election within 16 months of incorporation, which is typically conducted on the same date as the Annual General Meeting (AGM). The maximum tenure for all directors and the CEO is up to three years, after which the company must conduct fresh elections

For example:

If the first election is held on 28 October 2023

The next election must be held on or before 28 October 2026

Annual Returns:

After holding the AGM and conducting elections, the company must report to SECP by filing:

Form A (Annual Return): Must be filed annually

Form 9: (Particulars of Directors and Officers, Including The Chief Executive, Secretary, Chief Financial Officer, Auditors, Legal Adviser)

Will required to file every three years usually for election of directors

Typically, in private limited companies, the CEO and directors remain unchanged for years and are simply re-elected.

The last date of filing is to 120 days after the end of fiscal year, usually the companies having year ended 30 June, the 120 is the October 28 so it must be filed before 28 October every year.

Note: This requirement does not apply to Single Member Companies (SMCs).

Filing of Audited Financial Statements

All Companies required to submit audited financial statements to the registrar. However, this requirement does not apply to private companies and SMCs with paid-up capital not exceeding PKR 1 million.

Event-Based Filings:

Form-9: Appointment, Cessation, or Change in Company Officers

Any changes related to the appointment, resignation, or removal of directors, officers, or auditors must be reported via Form-9 within 15 days of the event.

Record of Ultimate Beneficial Owners (UBO)

Refers to a natural individual, not a company or organization, who directly or indirectly owns at least 25% of the company’s shares. All corporations are required to submit all of these facts to the SECP by completing either Form 7, 8, or 9, whichever is applicable. If a corporation fails to complete these forms, it may face fines of up to 500,000, indicating that it has committed a major offense.

Registered Office Address

All companies must maintain a registered office address. If a correspondence address was provided at the time of incorporation, then the company must update its official registered office address with SECP within 30 days of incorporation.If the address changes:

Use Form-21 for changes within the same province (e.g., Lahore to Faisalabad)

For inter-provincial changes, the company must also update its Memorandum and Articles of Association

Other Important Forms

In certain cases, such as when a company needs to make changes to its share capital, transfer shares to existing or new shareholders, or convert from a private limited company to a Single Member Company (SMC) and vice versa the following forms must be filed:

Change in Authorized Capital:

A company with share capital can make certain changes to its share structure if its Articles of Association allow and it passes a special resolution. These changes may include:

(a) Increasing its authorized capital to any amount it thinks necessary.

(b) Combining and dividing all or part of its shares into larger-sized shares.

(c) Splitting its shares into smaller-sized shares than mentioned in the original documents.

(d) Cancelling shares that have not yet been taken or agreed to be taken by anyone, and reducing its share capital by that cancelled amount.

If the company consolidates or splits its shares, the rights of the new shares must remain equal to the original ones.

Form-7 and Form-3

Also, if the company issues new shares of the same type as existing shares, then these new shares will have the same rights as the old ones. then it must file Form-7 (Notice of Alteration in Share Capital) and Change of More Than Twenty-Five Percent in Shareholding:

In cases where there is a change exceeding 25% in shareholding, the company must file Form-3.

Late Filing Penalties For SECP Forms

Penalties for delays in SECP Post-Incorporation Compliance for Companies are calculated as per the Updated-Seventh-Schedule-of-Companies-Act-2017, using the following formula:

| Delay Duration | Total Fee = Normal Fee + (Normal Fee × Multiplier) | Total Fee |

| Within 90 days | Normal Fee + (Fee × 2) | 1,210 + (1,210 × 2) = Rs. 3,630 |

| Within 180 days | Normal Fee + (Fee × 3) | 1,210 + (1,210 × 3) = Rs. 4,840 |

| Within 1 year | Normal Fee + (Fee × 4) | 1,210 + (1,210 × 4) = Rs. 6,050 |

| Within 2 years | Normal Fee + (Fee × 5) | 1,210 + (1,210 × 5) = Rs. 7,260 |

Simplified Guide for SECP Annual Filing in 2025 : Final Remarks

- Appointment of First Auditor required within 90 days if paid-up capital is more than 1 million.

- AGM: Most hold in the first 16 months then after 120 days of the financial year.

- Returns: Form A every year, Form 9 (For election) every 3 years.

- Audit Accounts: Mandatory for companies with capital more than 1 million.

- Change of address: Submit the form-21 within 15 days.

- Form-9 In case of any change in officer, director, CEO etc.

- UBO Details: Reporting of owners holding 25% or more shares is mandatory.

- For late filing Fee can increase by 5 times.

- Please contact us through our website by filling out the Contact Usform, or reach out via our social media accounts