Major Relief No Tax on Personal Cars and Assets FBR 2025 Simplified Guide

If tax is levied on the transaction of a personal used vehicle, how much tax you may have to pay and what payment you have to make to the FBR.

What is the tax treatment of the purchase and sale of a vehicle ?

If you get a profit on selling a vehicle, is it taxable or exempt, how much tax will you have to pay on it? and where to declare it in the income tax return?

Tax on sale of vehicle

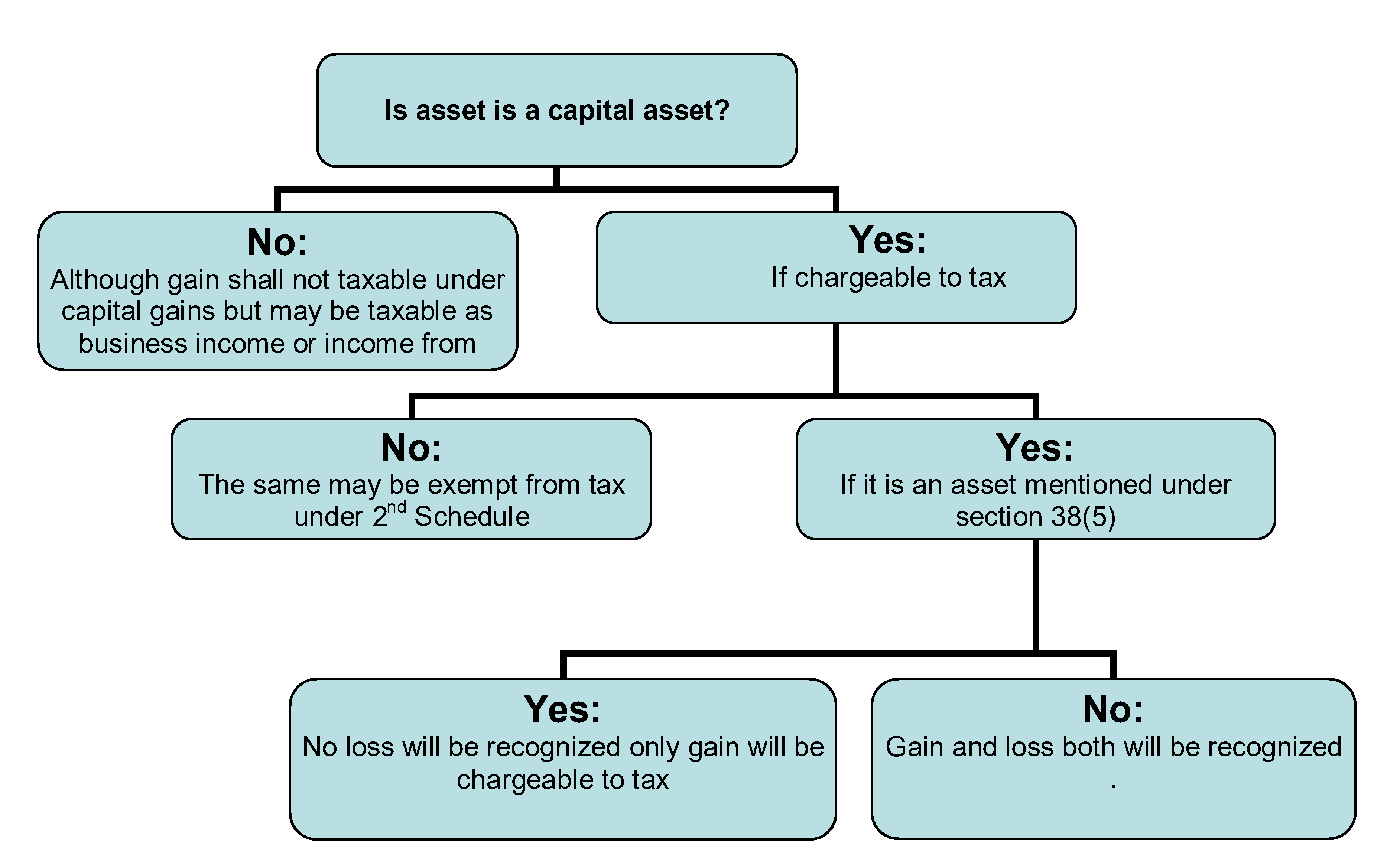

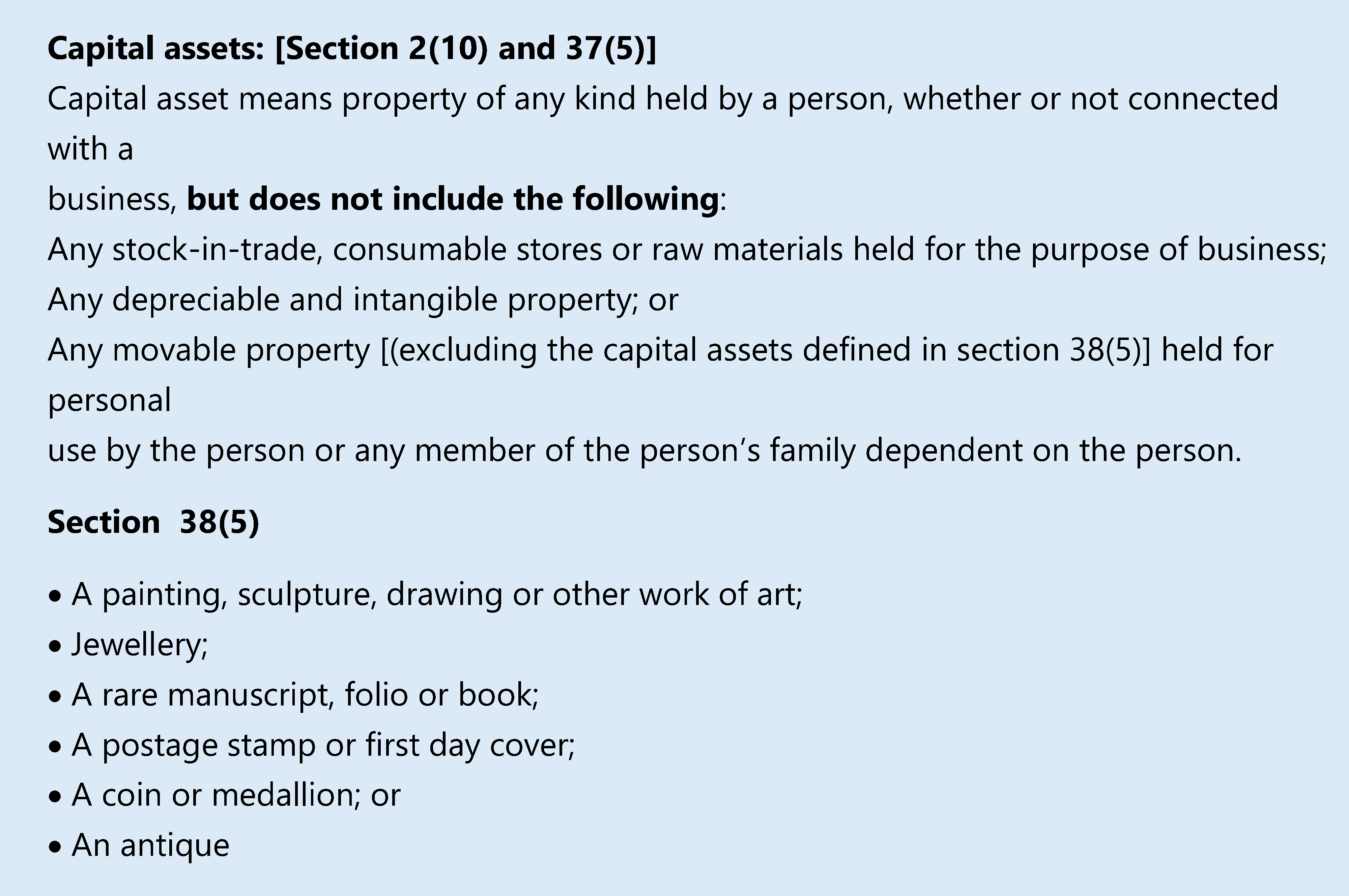

The capital asset is the property of any kind both movable and immovable which includes land, house, gold, cars etc.

Generally, whenever a capital asset is sold at a profit, capital gains tax is levied on the income earned. However, there are some cases where capital gains tax is not applicable on this profit.

Stock in Trade

The first case is that of stock-in-trade. If what you are selling is part of your normal business, then the income earned from its sale will not be considered capital gain but business income.

Therefore, it will not be subject to separate capital gains tax but will be included in the normal business income.

For example, if you are running a car showroom and you sell the cars in the showroom, the revenue earned from their sale will be business income, not capital gain.

Because these cars are stock-in-trade for you, not capital assets.

Income from Business is taxed differently

If you are a company, then the normal corporate tax rate will apply.

If you are an Individual, Partnership or AOP, then you will be taxed as per slab rates.

The slab rate depends on your total income the higher the income, the higher the tax.

So the first conclusion was that:

If buying and selling cars is your business like a showroom, dealership or car manufacturing company then its profit will be taxed as Business Income.

Personal Used Assets

If the capital assets is held for personal use by you or your dependent family members, the gain on the sale of the asset is generally not taxable. For example, on the sale personal used car.

Although profit earned on sale of personally used assets are exempted , there are some assets that will be subject to tax if a profit is made on their sale, including: such as Jewellery, painting, sculpture, other work of art, antique , coin or medallion.

How will the declaration be made in the return?

Where to show it in the income tax return?

If the vehicle is a business asset then It is a very simple method.

You can declare it under the Income from Business

If the vehicle was a Personal Asset (Exempt Case)

This is where most people get confused.

Since this is not income, it will not be included in the income of the Income Tax Return.

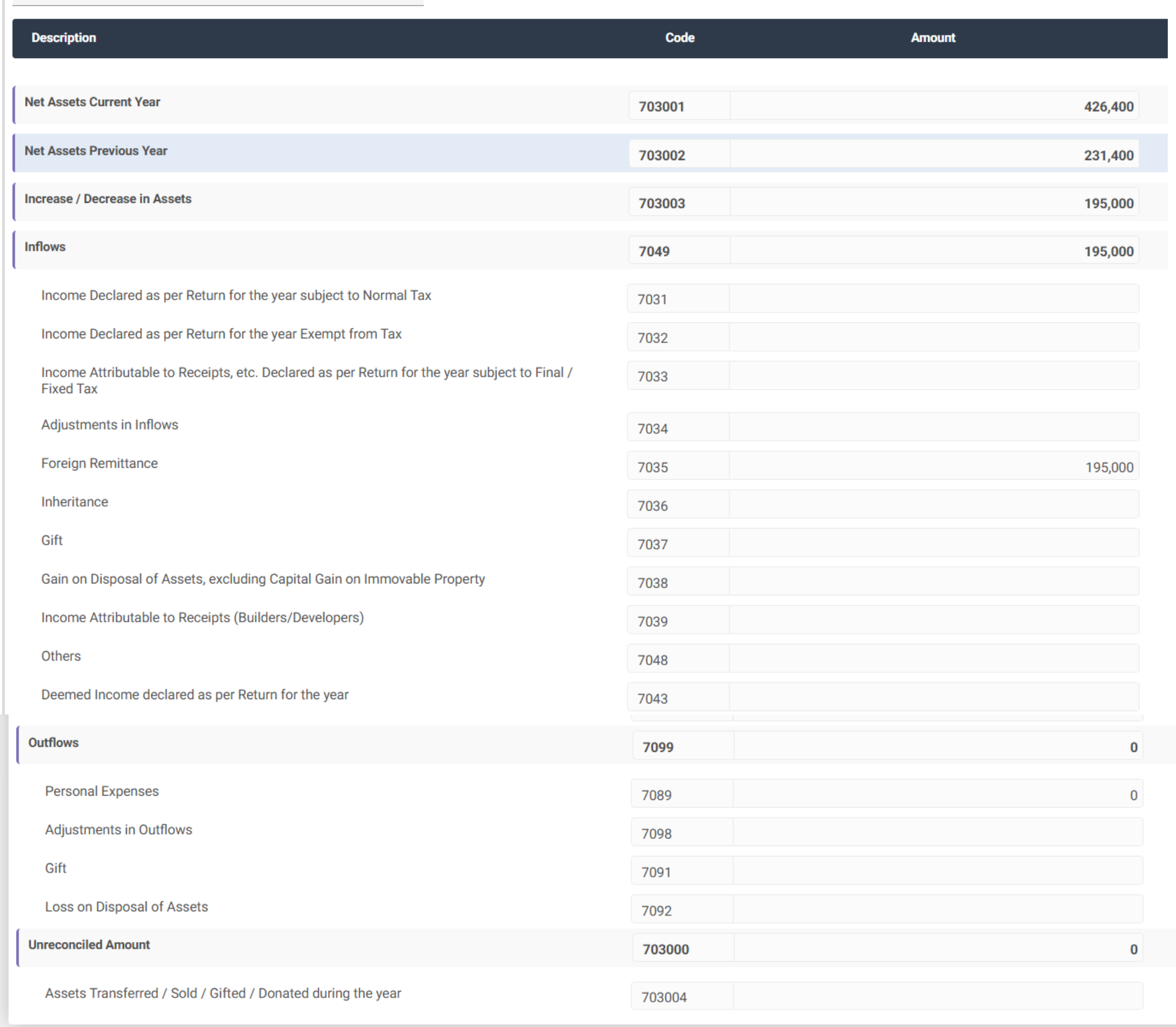

Rather, it will be shown in the Wealth Statement.

The Wealth Statement has three sections:

Personal Expenses

Personal Assets

Reconciliation Statement

How To Declare Assets Sold in Wealth Statement

Now the question is, if we have sold an asset, for example, a car, how should it be declared in the wealth statement?

There are a few possible scenarios for this. If we receive all the money from the sale price, then we either use that money to purchase a new one, or it is available with us in the form of cash or bank balance, or we spend it on personal expenses.

Personal Expenses or Purchased New Asset

If the money is spent on personal expenses, it will be declared in the Personal Expenses section.

If a new item is purchased with the same amount, for example, if we sell an old car and buy a new car, then the details of the newly brought car will be added to the Assets section.

And if this money is available with us, it will be shown in the Bank Balance or Cash in Hand.

How to Declare Profit/Gain or loss on sale of asset

After this, the next step is to see whether there is a profit or loss on the sale.

For example, if we bought some furniture for Rs. 10 lakh and sold it for Rs. 12 lakh, there will be a profit of Rs. 2 lakh.

This profit will be shown as Profit on Disposal of Asset in the Statement of Inflows.

If the same furniture is sold for Rs. 8 lakh, there will be a loss of Rs. 2 lakh, which will be declared Loss on Disposal of Assets in the Statement of Outflows.

Case law example:

In this case, the court clarified that assets held for personal use cannot be taxed. If you also receive such notices or are working as a consultant, you can refer this case and present it before the FBR or the relevant courts.

Appellate Tribunal decision regarding tax on sale of personal use vehicles

The matter before the Appellate Tribunal Inland Revenue, Islamabad, related to the tax year 2023 in which the taxpayer had sold two motor vehicles for personal use. The FBR officers had increased the assessment by declaring the proceeds of sale of the vehicles to be taxable under Income from Other Sources (Section 39) of about Rs. 78,80,000.

The taxpayer argued that these vehicles were movable property for personal use, hence the profit derived from their sale was not taxable even under the category of capital gains because as per Section 37(5) of the Income Tax Ordinance 2001, movable property for personal use (other than jewellery) does not come within the definition of capital asset.

Tribunal Decision

The Tribunal ruled that:

A motor vehicle for personal use is not a capital asset.

Therefore, the profit derived from its sale is not taxable under Section 37.

Moreover, such income cannot be taxed under Section 39 (Income from Other Sources).

Therefore, the Tribunal declared the increase made by the FBR illegal and quashed it and allowed the taxpayer’s appeal.

For further information Major Relief No Tax on Personal Cars and Assets FBR 2025 Simplified Guide please reach out via our social media accounts